In this how to record cash payments in Quickbooks guide, we will go over the advantages of Quickbooks and why it’s important for every business owner to know the tax laws and how to work with the tool for their advantage.

It is undeniable the effects of the pandemic on the world’s economy. With the hit of pandemic coronavirus COVID-19, many businesses had to adapt to a new reality, others merged, others unfortunately disappeared. Today’s economy is making it even harder to run a business.

This is why keeping accounting of your business has become imperative, especially if it is a small business. Most owners of small businesses usually fail to understand the importance of keeping their business accounting. Sometimes, they do not even understand what their accountant might be doing, like the tax return filed on a cash basis, for example.

Paperwork might be unpleasant, especially because it usually produces frustration and irritation. But there’s a good reason for paperwork to exist. When it comes to small business, whoever runs a small business must be aware of it.

If this is your case, don’t worry. There is no need to have a Master’s Degree in accounting in order to keep your business books. But it is important to at least understand the importance of keeping it in order to make future decisions.

Luckily, there are ways to manage your business income and expenses. QuickBooks is one of the best and most popular options as it is a small business accounting software. Quickbooks offers you the possibility to make several operations to manage your business books.

How to Record Cash Payments in Quickbooks

From tracking everyday expenses to cash flow to sending invoices, Quickbooks is dedicated to helping small business owners get their business going. Even if you know nothing about accounting, Quickbooks is there to help you build your business.

It is easy and almost intuitive to use. However, there’s a common question users usually have about Quickbooks: how to record cash payments? Today, you are going to finally get the answer.

Small Business Accounting Method

When it comes to bookkeeping and tax filing, the business account method that you choose for your small business is essential. Why? Because the accounting method will affect the way income and expenses are recorded on your books and thus in the tax year transactions.

However, choosing a method over the other sometimes isn’t just the business owner’s call. For example, in the U.S. the Internal Revenue Service (IRS), the government department responsible for collecting taxes encourages owners to use a standardized and consistent accounting method each year to file small business taxes.

In fact, if you choose an accounting method and then decide to change it to the other, you must get the IRS approval. If the IRS rejects your request of changing the method, you might end up being fined for underpaying taxes.

Besides, in the U.S. publicly traded companies must use accrual accounting according to what is commonly accepted by the GAAP (which means Generally Accepted Accounting Principles). Fortunately, this does not affect small businesses. These last have significantly more freedom to choose which method to use.

Basically, keeping your business legal and running requires some form of consistency. This is why selecting a specific accounting method will help your company to succeed financially and legally, not to mention it will help you make better decisions.

Now, let’s get into the differences between cash vs. accrual accounting.

Using Cash Basis Accounting

Cash basis accounting is probably the simplest way to keep a record of your small business. In cash basis accounting, income is recorded when received and expenses are paid. Cash basis accounting is a very useful accounting method, bringing several benefits:

- When starting a business, many people usually go as a solopreneur. For this reason, when using cash basis accounting, you are going to be the sole proprietor. In fact, it is the ideal method for entrepreneurs to keep many responsibilities at the same time in motion. It offers simplicity for people who can’t afford an accountant for their small businesses.

- It helps you prepare for tax season. Cash basis accountant facilitates paying your business taxes since it actually represents how much money you have on hand. It also gives you flexibility when it comes to filing this year’s taxes. If there is an expense you didn’t report before the deadline, you can always report it next year’s report using this accounting method.

Using Accrual Accounting

In accrual basis accounting, income is recorded when earned and expenses are incurred.

Even though cash basis accounting is way simpler, many businesses need to use accrual accounting. For instance, if your business has average gross revenue of over $25 million during a three-year period, you are required to use accrual accounting. Businesses with an inventory are also required to use accrual basis accounting.

Nonetheless, accrual accounting also has some advantages:

- Though cash basis accounting is easier, accrual accounting is usually the preferred method since it offers a more precise representation of your business finances. Its key metrics are more stable, making it possible for your finances to be more consistent.

- Not to mention, accrual accounting, as aforementioned, is accepted by the GAAP, making it a best practice.

- If you are looking to apply for outside funding, accrual accounting is the best method to choose.

A hybrid method

Choosing an accounting method might be tricky. The good news is that you can merge both methods into a hybrid method. How do you do it?

You may file your tax return using cash basis accounting while reviewing your financial statements on an accrual basis accounting. Doing this is completely acceptable. In fact, some experts recommend using a hybrid method when managing business finances.

What is Quickbooks

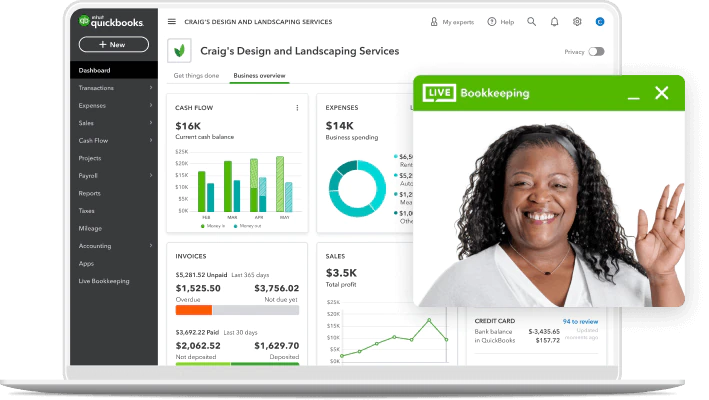

QuickBooks is the most popular small business accounting software businesses use to manage income and expenses and keep track of the financial health of their business. It offers several financial operations like invoicing customers, paying bills, generating reports, and preparing taxes.

Quickbooks functions

From managing invoices, paying bills, and keeping track of cash flows, Quickbooks offers small businesses owners numerous functions to facilitate them bookkeep their business finances.

- Small business owners use Quickbooks to create and track invoices. Quickbooks makes it even easier: it automatically records the income and tracks how much each customer owes you.

- Quickbooks allows you to keep track of bills and expenses connected to your back and/or credit cards. Quickbooks automatically categorize your expenses by transactions made. You can also track upcoming payments, so you’ll never forget to pay your bills.

- Quickbooks provides the option of printing your business financial statements when you report your cash inflow and outflow activities.

- You can access a profit and loss report with Quickbooks. This way you are able to analyze how profitable your business is by deducting your business income minus its expenses.

- Quickbooks also provides a balance sheet report which shows you the assets, the liabilities (owes), and your business net worth (equity). Another report Quickbooks provides is the cash flow statement which shows the cash inflows and outflows activities.

- It helps you keep track of inventory which is very helpful if you’ve chosen an accrual basis accounting for your small business.

- Another benignity of Quickbooks is that it simplifies taxes, being this perhaps the most important feature Quickbooks has.

As already stated, Quickbooks is a great option for small business accounting since it is an all-in-one platform. It allows you to manage it all from one place. In Quickbooks, you are able to perform different tasks which will help you not only keep track of your business financial situation but also understand your business’s finances.

The step-by-step to enter cash payments in QuickBooks

Since cash transactions are way far from disappearing, Quickbooks also offers small business owners the option to record cash payments. And it is a simple process too.

Keep in mind that only sales receipts are recorded in Quickbooks. Try doing it on the same day to avoid future inconveniences.

Let’s get through the steps of how to record cash payments first in the desktop format of Quickbooks and then we’ll get into the online format.

Desktop QuickBooks

- Login in to your Quickbooks account and go to the Banking menu.

- In the options click on Make deposits, then select Payments to Deposit. A list will prompt, click on the cash payment option and choose OK.

- Select the bank account where the money will be deposited. Click Deposit To. Fill in all the information required: date, details, cash amount, etc. You are able to enter several cash amounts since Quickbooks will automatically sum them up.

- If you want to keep a paper record of this transaction, you must click on the Print Button.

- Finally, save your cash deposit by clicking Save and Close.

Online Quickbooks

The online format of Quickbooks offers two ways to record your cash payments.

Through a sale receipt

- Login to your Quickbooks account and on the + button.

- Click on Sales Receipt. A drop-down list will show up, select Customer.

- Fill in all the required information for the transaction.

- Then go to Deposit To option, select the bank account where the money will be deposited.

Through a bank deposit

- Login to your Quickbooks account and on the + button.

- Click on Bank Deposit. A drop-down list will show up, select Account.

- Select the bank account where the money will be deposited.

- In the deposit section, you’ll see an Add Funds option, click on Received From and enter the income amount.

- Finally, save your cash deposit by clicking Save and Close.

The bottom line

Quickbooks is a software that offers numerous advantages for small business owners to carry out and keep records of their business financial transactions. It makes owners feel sure their books are accurate. And as small businesses usually receive payments in cash, it is important to know the how-to when making those records in Quickbooks in order to keep their businesses’ accounts updated.